A snapshot of where the world’s young founders are, what they are building, how they are funded, and what AI is changing.

Three numbers that frame this moment

| #1 For the first time, U.S. 18 to 24 year olds are tied with 25 to 34 year olds as the most entrepreneurially active age group, at 25% TEA (GEM 2024) | 2.5x Increase in U.S. youth early-stage entrepreneurial activity over the past decade, from approximately 10% to 25% (GEM USA, 2013 vs 2024) | ~30% Outperformance of investments in under-25 founding teams versus older peers, per First Round Capital’s 10-year analysis |

Sources: Global Entrepreneurship Monitor (GEM) USA, 2013 and 2024 cycles (Total early-stage Entrepreneurial Activity, or TEA, by age group); First Round Capital, 10 Years of Tracking Founder Demographics, 2015.

Key findings

- Youth founding is now mainstream across advanced economies. In the United States, 18 to 24 year olds are tied with 25 to 34 year olds at 25 percent TEA (Total early-stage Entrepreneurial Activity, the Global Entrepreneurship Monitor’s primary indicator) for the first time since GEM began measuring it. The same upward trajectory is visible in the UK, Canada, Australia, and the Netherlands. In most emerging economies, youth TEA runs higher still, but is driven by a fundamentally different mix of necessity and opportunity.

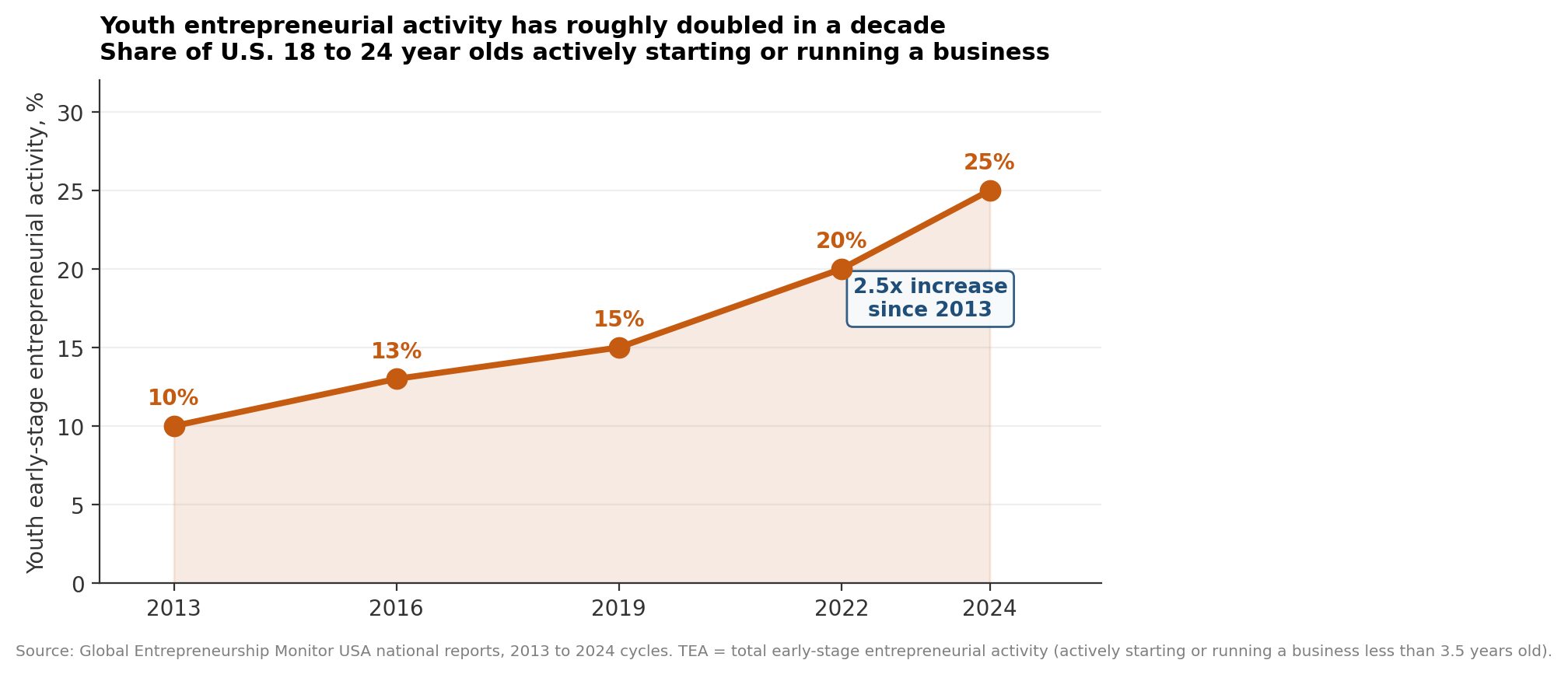

- Activity has roughly doubled in a decade. U.S. youth TEA has risen from approximately 10 percent in 2013 to 25 percent in 2024, with similar directional trends across the UK, Canada, and multiple emerging economies.

- Young founders are overrepresented in five categories: AI tooling and software, creator and content businesses, services and freelancing, direct-to-consumer commerce, and mobile-first services filling institutional gaps. Climate interest is high but rarely converts into actual ventures.

- Most are not venture-funded. The typical under-25 founder in 2026 is bootstrapped or revenue-funded, often running a services or creator business, and is under-served by every institution that writes about startups.

- The geographic center of gravity is shifting toward Asia and Africa. Africa’s population is projected to nearly double by 2050 with most growth under age 25, and India and Southeast Asia already have high rates of youth venture creation.

- Youth entrepreneurship is not a single phenomenon. Necessity-driven founding dominates in most emerging economies; opportunity-driven founding dominates in advanced ones. Inside opportunity-driven entrepreneurship, access is gated by family wealth and elite educational networks.

- AI is compressing the minimum viable team toward one. The solo founder is becoming the norm among the youngest cohort, not the exception.

- The field has a measurement problem. Most sources begin measurement at age 18, so founders 15 to 17 are almost invisible in official data. No major dataset tracks survival or revenue outcomes for under-25 founders at scale. Formation activity is visible while durable outcomes are not. That is the gap the next generation of research, programs, and policy should close.

Starts have surged; outcomes are lagging

Youth entrepreneurship in 2026 is a large and growing global phenomenon. Activity rates among 15 to 24 year olds have roughly doubled in several major economies over the past decade. Young founders are concentrated in software, creator, and service categories, most are funded outside of venture capital, and artificial intelligence is compressing what a single founder can build fast enough to reshape who becomes a founder. The drivers are cultural, economic, and technological, and the geographic center of gravity is shifting toward Asia and Africa.

But the aggregate numbers hide important divergences: youth founding is necessity-driven in most emerging economies and opportunity-driven in advanced ones, the opportunity itself is gated by family wealth and elite educational networks, and legal and immigration barriers shape who can build where.

Activity is rising faster than measurable outcomes. The supply of young people starting something has outpaced the institutional scaffolding that converts starts into durable businesses. That gap is both the central challenge and the central opportunity. This report maps the landscape: who is starting, what they are building, how they are funded, why now, and what comes next.

1. Activity has doubled; geography is shifting

Youth entrepreneurial activity is rising in virtually every economy that measures it, and the rate of increase has accelerated since 2020. The most striking data point comes from the United States, where the share of 18 to 24 year olds actively starting or running a business roughly doubled over the past decade, from approximately 10 percent in 2013 to 25 percent in 2024. That 25 percent ties them with 25 to 34 year olds as the most entrepreneurially active age group in America for the first time in the Global Entrepreneurship Monitor’s measurement history. The United Kingdom’s youth TEA reached a record 13.7 percent in the most recent GEM cycle, and other advanced economies including Canada, Australia, and the Netherlands have trended upward over the same period. The trend is visible across both advanced and emerging economies, though it starts from different baselines and reflects different underlying motivations.

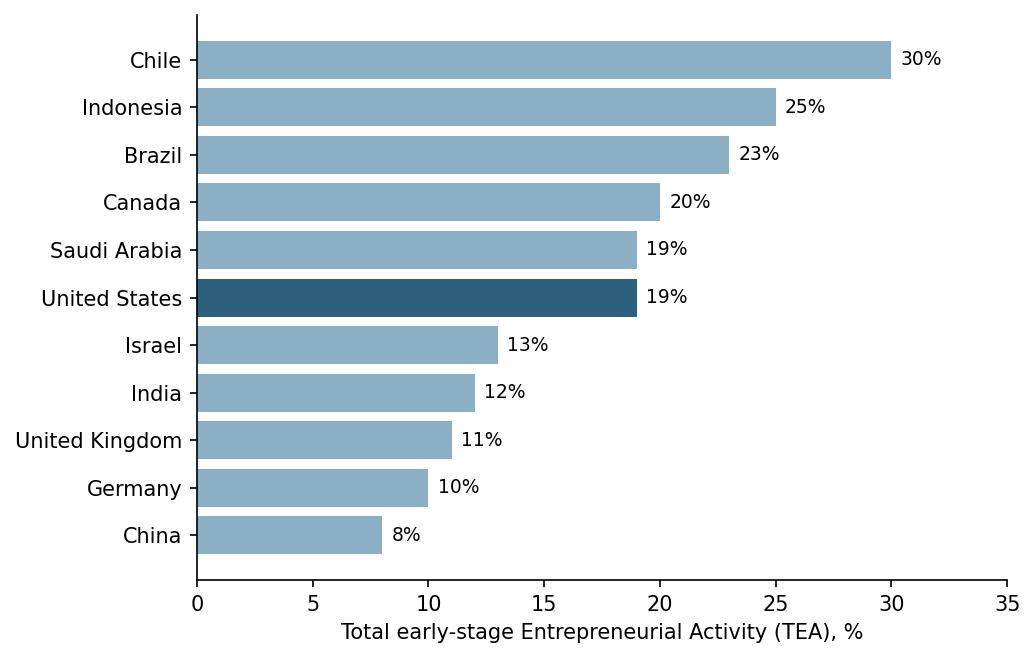

The US sits in the upper-middle of advanced economies

Youth-specific TEA data is published in depth only for a handful of economies, but overall TEA rates from the most recent GEM cycle show the wide spread in entrepreneurial intensity across advanced and emerging markets. Latin America and select Gulf states lead on overall activity; Western European and East Asian economies sit lower; the United States sits in the upper-middle of advanced economies and, uniquely, is now led by its youngest cohort.

Tens of millions active; gender, race, and geography all shifting

Precise global headcounts do not exist, but the scale is large. When GEM’s published youth TEA rates are applied to the UN’s estimate of roughly 1.2 billion people ages 15 to 24 worldwide, they imply tens of millions actively building businesses, with the large majority in emerging markets. The gender gap, while persistent, is narrower among youth than among older founders: across OECD (Organisation for Economic Co-operation and Development) countries, young women’s TEA rate was 9 percent versus 11 percent for young men in the most recent measurement period, and the gap has been steadily closing. Racial and ethnic composition has also shifted: according to Kauffman Indicators of Entrepreneurship, the share of new U.S. entrepreneurs who are Latino rose from 10 percent in 1996 to roughly 24 percent in 2021, the Black share rose from 8 to about 10 percent, and the Asian share rose from 3 to 7 percent. These figures are for new entrepreneurs overall rather than youth specifically, but the youth cohort follows the same directional trend.

The geographic center of gravity is shifting. Africa’s population is projected to nearly double by 2050, and the large majority of that growth will be among people under age 25. India, Indonesia, and much of Southeast Asia already have high rates of youth venture creation. By 2035, on current trajectories, the majority of the world’s young entrepreneurs will be building in economies that today’s mainstream entrepreneurship coverage barely mentions.

Necessity abroad, opportunity at home, privilege filters both

Youth entrepreneurship is not a single phenomenon. GEM data consistently shows a split between necessity-driven founding, where young people start a business because the formal labor market has no room for them, and opportunity-driven founding, where they start because they see an opportunity. In most emerging economies, the majority of youth TEA is necessity-driven. In advanced economies, it is predominantly opportunity-driven. The distinction matters because the support these two groups need is different: an unemployed 22 year old in Lagos running a microenterprise and a 22 year old at Stanford shipping an AI tool appear in the same aggregate statistic but face entirely different constraints. A second filter operates inside opportunity-driven entrepreneurship. Being able to spend two years unpaid on a venture is itself correlated with family wealth, access to parental health coverage, student-loan deferral, and elite educational networks. The visibility of spectacular young founders masks how much of the opportunity is gated by privilege.

More attempts while young, and more unique trade-offs

The relationship between starting age and outcomes is nuanced. Stanford research on serial entrepreneurs finds an 82 percent revenue jump between a founder’s first and second venture, suggesting that early starts create more time for the iterations that build skill. At the same time, MIT and National Bureau of Economic Research (NBER) research finds that the average age of founders behind the fastest-growing startups is 45, and mid-career founders are more likely to build durable businesses on any single attempt. The advantage of starting young is not that any individual venture is more likely to succeed; it is that early founders get more attempts while personal risk is low.

Youth entrepreneurship also carries a structural trade-off that older founders do not face: the decision to continue or leave formal education. Many of the most visible young founders built their companies while enrolled, or left school to pursue a venture full-time. That choice shapes timing, networks, and risk in ways unique to this age group. It is compounded by legal and institutional barriers that vary by country: in many jurisdictions, founders under 18 cannot sign contracts, open business bank accounts, or raise capital without parental involvement. These frictions do not appear in TEA data, but they shape the landscape. For international young founders building in the United States, immigration constraints compound the problem: F-1 student visa rules effectively prohibit full-time founding while enrolled, the International Entrepreneur Rule has been volatile across administrations, and H-1B (specialty occupation work visa) lotteries exclude most first-time founders. Many of the most ambitious young founders from abroad either build elsewhere or incorporate in their home country while remaining enrolled at a US university.

2. Software, creators, and services dominate; climate ambition exceeds formation

Young founders are concentrated in different sectors from the broader small-business economy, which skews toward services, construction, food, and retail. Founders under 25 are overrepresented in software, creator, and digitally native categories, and underrepresented in capital-intensive and licensing-heavy sectors. Five categories dominate:

- AI tooling and software. The fastest-growing category. Young founders are building agents, code assistants, vertical SaaS (software as a service), and developer tools at rates that exceed their representation in general startup formation, driven by fluency with language models and low marginal cost of software delivery.

- Creator and content businesses. YouTube channels, newsletters, Substacks, TikTok storefronts, and Patreon practices run as businesses. Under-25 founders are overrepresented here versus any prior cohort at the same age, and these ventures are frequently the first formal income a founder earns.

- Services and freelancing operated as businesses. Design studios, marketing practices, development shops, and consulting operations formalized through platforms like Upwork, Fiverr, and Contra. Often the bridge between employment and a product company, and the single largest category of youth entrepreneurship by headcount.

- Direct-to-consumer and e-commerce. Shopify stores, print-on-demand brands, and small physical-product companies. A maturing category with a widening survival gap between founders who master paid acquisition and those who do not.

- Mobile-first services filling institutional gaps. Fintech, logistics, education, agritech, and mobile-native consumer services, concentrated in India, Southeast Asia, Africa, and Latin America, where young founders build for needs that larger institutions have not addressed. In many emerging economies, this is the largest category of youth venture creation.

Climate and sustainability ventures attract disproportionate interest from younger cohorts, but that interest rarely translates into actual ventures. Deloitte’s 2024 Gen Z and Millennial Survey found that 62 percent of Gen Z worry about climate change, 54 percent are pressuring employers to act on it, and one in five has already changed jobs over environmental concerns. The gap between that level of concern and the modest share of youth venture formation in climate categories is itself a signal: capital intensity, technical complexity, and long payback cycles continue to filter out the youngest founders even on the problem they rank among their top concerns. Hardware and deep-technology ventures remain underrepresented among the youngest founders for the same reasons.

3. Bootstrapped capital, uneven support, unmeasured outcomes

Most young entrepreneurs operate outside institutional capital. The large majority of under-25 ventures are bootstrapped, revenue-funded, or financed through small personal networks; raising outside equity remains rare.

Young teams get little venture capital, but outperform by 30 percent

Global venture capital deployed was approximately $368 billion in 2024, per KPMG. Teams composed solely of founders under age 25 receive a small share of that total, though the share has been rising modestly each year as more founders fluent in AI tooling enter the market. First Round Capital’s 10-year analysis found that investments in under-25 founding teams outperformed older peers by approximately 30 percent, suggesting that young founders, when funded, deliver outsized returns. The geographic concentration is extreme: the United States, United Kingdom, Israel, and China together account for the large majority of venture capital going to young founders, even though those countries represent a small minority of the world’s young entrepreneurs.

Accelerators and student funds: small dollars, outsized early-stage influence

Y Combinator (YC)’s under-25 batch representation has been rising for several years; Pioneer, Neo, and Contrary run programs explicitly oriented toward young and student founders. Student-run and student-adjacent funds (Dorm Room Fund, Rough Draft Ventures, Pear VC’s fellows program) write small checks at the pre-seed stage and have grown meaningfully in number and deployment since 2020. Together, this layer moves hundreds of millions of dollars annually; it is an order of magnitude smaller than later-stage venture but disproportionately influential in shaping the earliest-stage pipeline.

Universities and programs are expanding, but concentrated in elite regions

Beyond capital, the institutional response has accelerated markedly since 2020. Babson, Stanford, MIT, Harvard, and a growing cohort of universities now operate dedicated student venture programs, pre-seed funds run by current students, and accelerators designed around undergraduate timelines. Entrepreneurship programs have also expanded downward: an increasing number of high schools offer formal entrepreneurship curricula or summer programs, and standalone programs (YC Startup School, BUILD, Network for Teaching Entrepreneurship, and a growing set of high-school-targeted accelerators) now reach tens of thousands of students annually. The supply of institutional scaffolding is growing, but unevenly: it is concentrated in elite universities and well-resourced regions, reinforcing the access question raised in Section 1.

Customer revenue is the largest source; venture capital is the outlier

The largest and fastest-growing capital source for young founders is customer revenue. Second is family and personal networks. Third is non-dilutive capital: grants, competitions, university programs, and a growing number of government-backed youth enterprise schemes. The venture-funded young founder is newsworthy but statistically rare; the typical young founder in 2026 is bootstrapped or revenue-funded, with a small product, and is under-served by every institution that writes about startups. No major dataset tracks survival or revenue outcomes for under-25 founders at scale, which is itself part of the problem: the gap between formation activity and durable outcomes remains largely unmeasured.

Six measurements the field is missing

Six measurements would transform what the field can say about itself.

- Five-year survival and revenue trajectories for under-25 founders, tracked from formation rather than inferred from funded outcomes.

- Outcome data disaggregated by necessity versus opportunity motivation, so that aggregate TEA does not conflate two fundamentally different phenomena.

- Program-level outcome tracking (revenue, employment, survival) for the rapidly growing youth accelerator and education ecosystem.

- Demographic breakdowns (race, ethnicity, socioeconomic background, immigration status, and age bands including under 18) consistent across countries, so that the access question can be measured rather than asserted.

- AI adoption and AI-assisted productivity metrics for young-founded companies, so that the compounding effect hypothesized in Section 4 can be verified or falsified.

- Formal measurement of the 15 to 17 founder band. Most sources begin measurement at age 18, rendering the youngest and fastest-growing cohort essentially invisible in official data.

None of these six measurements are technically hard to build. They are simply not yet prioritized.

4. Four waves compressed the viable team toward one

The four waves that shaped this moment: Internet (1995) → Mobile (2008) → Social (2012) → AI (2023). Each wave lowered the barrier to founding and produced a younger cohort of builders.

Cultural. Founding a company has moved from an eccentric career choice to an aspirational default among young people in most advanced economies, well above what prior generations reported at the same ages. Social media has accelerated the shift. The visibility of young founders on TikTok, Instagram, YouTube, and X has normalized the path: an 18 year old in 2026 sees peers building companies daily in a way no prior generation did at the same age. Founding has become both more aspirational and more legible. The mechanics of shipping a product, raising capital, and building an audience are now performed publicly by people of the same age, which lowers the perceived strangeness of trying. Among U.S. workers, 57 percent of Gen Z report running a side hustle (including gig work and freelancing), compared with just 21 percent of Boomers, per The Harris Poll. Not all of this is entrepreneurship in any formal sense, but it signals a generational shift toward self-directed income.

Economic. Real wage growth for young workers in advanced economies has been weak while housing and education costs have risen, making traditional career paths less attractive relative to building something of one’s own. In emerging economies, the economic push is even sharper, as described in Section 1. The economic driver is the structurally most important of the four, and the least celebrated.

Technological. Each wave of infrastructure, from consumer internet to mobile to social platforms to no-code tooling, lowered the cost and skill required to ship a product. Social media in particular gave young founders a native channel for audience-building and customer acquisition that did not require credentials or professional networks. Each wave produced founders who started younger, with smaller teams, and with less capital.

AI (the fourth wave). Commodity language models and coding assistants are compressing the minimum viable team toward one. A 19 year old in 2026 can ship a working SaaS product, landing page, and billing flow in a weekend; the same task in 2015 required a small team and several months. The marginal cost of starting something has fallen toward zero for a widening range of software, content, and services. For young founders, who treat AI tooling as a baseline assumption rather than a novelty, the effect is compounding: each generation of models widens the gap between what one person can build and what required a team just a few years earlier. The solo founder is no longer an outlier among the youngest cohort; it is becoming the norm.

5. Four archetypes; spectacular extremes mask a quiet middle

Young founders are not a monolith. Four archetypes recur across geographies and cohorts, each reflecting a distinct driver and advantage of starting young. These are patterns, not probabilities; for every founder who raises venture capital or scales to millions in revenue, thousands more are running small, underfunded ventures with limited support. Four LaunchX alumni and one additional founder illustrate the range; LaunchX affiliation is disclosed where applicable.

The technical innovator. Edward Tian, LaunchX 2015. Built GPTZero as a Princeton senior project in January 2023, turning a weekend prototype into the leading AI-detection platform within weeks and raising 3.5 million dollars in seed funding by mid-2023. Technical innovators lead with a technology that did not exist before; their youth advantage is native fluency with the frontier. Tian shipped in days what an established company would have taken months to scope.

The market scaler. Aadit Palicha, LaunchX 2019. Born in 2001, co-founded Zepto at 19, building an Indian quick-commerce grocery delivery company. By 24, he was running a company valued at 7 billion dollars, having raised over 2 billion dollars in total funding. Market scalers identify a massive underserved market and move on it at an age when personal risk is lowest. The pattern spans geographies and funding models: Ben Francis founded Gymshark in England at 19, bootstrapped it for eight years, and grew it to over 1 billion dollars in valuation. The technology may not be novel, but the speed, ambition, and willingness to bet everything on a market opportunity are distinctly young.

The impact builder. Annie Lu, LaunchX 2017. Left Harvard at 20 to co-found Laminar (formerly H2Ok Innovations) with her brother David. Laminar uses proprietary spectral sensing and AI to help CPG (consumer packaged goods) manufacturers like Unilever, Coca-Cola, and Danone run faster, more sustainable factories, reducing water, energy, and chemical usage by 10 to 20 percent. The company has raised over 19 million dollars, with a Series A led by Greycroft. Impact builders lead with a problem they want to solve for the world. Their youth advantage is idealism backed by technical skill, and a willingness to tackle hard science problems before the market tells them it is too difficult.

The serial builder. Harshita Arora, LaunchX 2017. Started coding at 13, shipped a crypto tracking app at 16, co-founded AtoB (Y Combinator Summer 2020), a fleet financial platform serving over 30,000 fleets, and in 2026 became YC’s youngest General Partner at age 25. Serial builders start so young that by their mid-twenties they have more venture attempts than most first-time founders at 35. Their advantage is not any single venture; it is the compounding effect of a decade of building, failing, and learning while personal risk is low.

The other end of the distribution: fraud, failure, and burnout

Any honest report on young founders has to acknowledge the other end of the distribution. The same conditions that produce spectacular early success also produce spectacular early failure. Theranos, FTX, and Frank are not youth-entrepreneurship stories per se, but they involve founders who started extremely young, built under intense public visibility, and carried more responsibility than their experience supported. More commonly and less visibly, young founders burn out, close ventures they cannot sustain, or spend their most formative years on companies that ultimately generate no traction. The spectacular success cases are real, and the spectacular failure cases are real. Most youth entrepreneurship happens between them, in quiet ventures that neither crash nor break out, and it is that middle that the field currently measures least well.

6. The future: more solo, global, and policy-divergent by 2030

- Solo founding will become the default for under-25 founders by 2028. AI tooling is compressing the minimum viable team toward one, and young founders, who adopt these tools fastest, will lead the shift.

- By 2030, the majority of the world’s young entrepreneurs will be in Asia and Africa, not North America or Europe, driven by demographic growth and rising mobile and AI access in those regions.

- The aspiration-activity gap will narrow materially in emerging markets (where tooling is the binding constraint) and narrow more slowly in advanced economies (where risk, regulation, and cost of failure are the binding constraints).

- Outcome data will create accountability pressure. As revenue, employment, and survival metrics for graduates’ ventures become easier to track, funders and participants will increasingly use them to compare youth entrepreneurship programs, making enrollment and satisfaction insufficient proxies.

- AI fluency will become an explicit screening criterion. By 2028, leading accelerators, student venture funds, and pre-seed investors will evaluate how effectively a founding team uses AI tooling as a standard part of diligence, much as product-market fit and unit economics are evaluated today.

- Policy divergence will become a key competitive variable among advanced economies. Nations that resolve immigration constraints on young founders, reduce the cost of a failed first venture, and broaden access beyond elite educational networks will capture disproportionate founder talent by the end of the decade. Those that do not will continue to lose their best young builders to jurisdictions that do.

7. Close the gap between starting and sustaining

The central challenge is no longer getting young people to start; it is helping them sustain. Formation activity has surged, but the scaffolding that converts a start into a durable business has not scaled proportionally: capital access, mentorship, distribution support, and institutional knowledge all remain thin for founders under 25. The support systems that exist were designed for founders with professional track records. Closing that gap is the structural opportunity.

For operators and investors. The highest leverage intervention is on the outcomes side, not the activity side. Tooling has solved formation; capital, distribution, and early-revenue support have not scaled to match. Programs, investors, and platforms that can reliably move a young founder from working product to sustained revenue will capture disproportionate returns.

For educators and institutions. Outcome tracking is becoming newly feasible and will reshape the field. As tools for measuring graduates’ revenue, employment, and venture survival improve, programs that report these metrics will attract disproportionate funding and talent. The shift from enrollment-based to outcome-based evaluation is already underway in adjacent fields; youth entrepreneurship will follow.

For policy makers. The binding constraint in most advanced economies is not desire to found; it is the cost of failure. Employer-tied health coverage, student debt, and rigid licensing regimes raise that cost asymmetrically for young founders. The credible policy lever is reducing the downside of a failed first venture, not celebrating formation that would happen anyway. A second lever, particularly in the United States, is immigration policy. F-1 student visa and OPT (Optional Practical Training) constraints exclude a generation of international students from founding while enrolled, and no dedicated founder visa pathway exists. The countries that resolve this will capture disproportionate young-founder talent over the next decade.

For young founders themselves. Start earlier than feels reasonable, ship before the product feels ready, and treat AI tooling as the baseline assumption about what one person can accomplish. The evidence is consistent: the founders who will look defining in 2030 are making their first serious attempt now, when the cost of doing so has never been lower. One caveat worth carrying into that attempt: the same conditions that make early founding possible also raise the personal cost. Young founders report higher rates of anxiety and burnout than older peers, and the cultural pressure to ship publicly and start earlier each year is real. Treat sustainability of the founder as seriously as sustainability of the venture.

The deeper story of this moment is not that more young people are starting businesses, though they are. It is that the minimum viable founder, the smallest possible person who can build something real, has gotten younger, more global, and more solo over the past fifteen years, and AI is accelerating the compression. The institutions that converted that activity into durable companies over the past several decades were designed for older founders with professional track records, and they have not caught up. The opportunity for operators, investors, educators, and policy makers is to build the scaffolding that the current generation is outrunning. The opportunity for the founders themselves is to build the companies that will define the next decade, while there is still time to learn from failing at one.

Methodology and sources

This report uses ages 15 to 24 as its primary band, following the UN and ILO (International Labour Organization) definition of youth. A young entrepreneur is anyone whose primary or significant work activity is building a business they own or co-own, whether or not it has revenue, employees, or outside capital. A data gap: most sources, including GEM and the OECD, begin measurement at age 18. Junior Achievement is the only major organization that tracks the 15 to 17 band, where it finds that 4 to 6 percent of teens have started a business. The 15 to 17 segment is therefore underrepresented in the data throughout this report.

Sources: Global Entrepreneurship Monitor USA national reports, 2013 to 2024 cycles (early-stage activity, ages 18 to 24); OECD The Missing Entrepreneurs reports, 2019 to 2023 (youth aspiration, activity, and gender gaps); International Labour Organization (labor market metrics and youth definitions); UN population projections; First Round Capital, 10 Years of Tracking Founder Demographics, 2015 (age-based investment performance); The Harris Poll for CNBC, 2023 (generational side-hustle data); Deloitte 2024 Gen Z and Millennial Survey (climate attitudes and workplace behavior); Kauffman Indicators of Entrepreneurship (race, ethnicity, and demographic trends among U.S. new entrepreneurs); PitchBook and Crunchbase (formation structure and capital flows). Where a single number is cited, the source is identified inline. Where an approximate or indicative figure is used, that is noted.

Disclosure: The author, Laurie Stach, is the founder of LaunchX and has a direct financial and reputational interest in four of the five founders profiled in the spotlight section. That affiliation is disclosed where applicable, and the report is constructed so that every non-profile claim is verifiable independently of LaunchX data or programs.